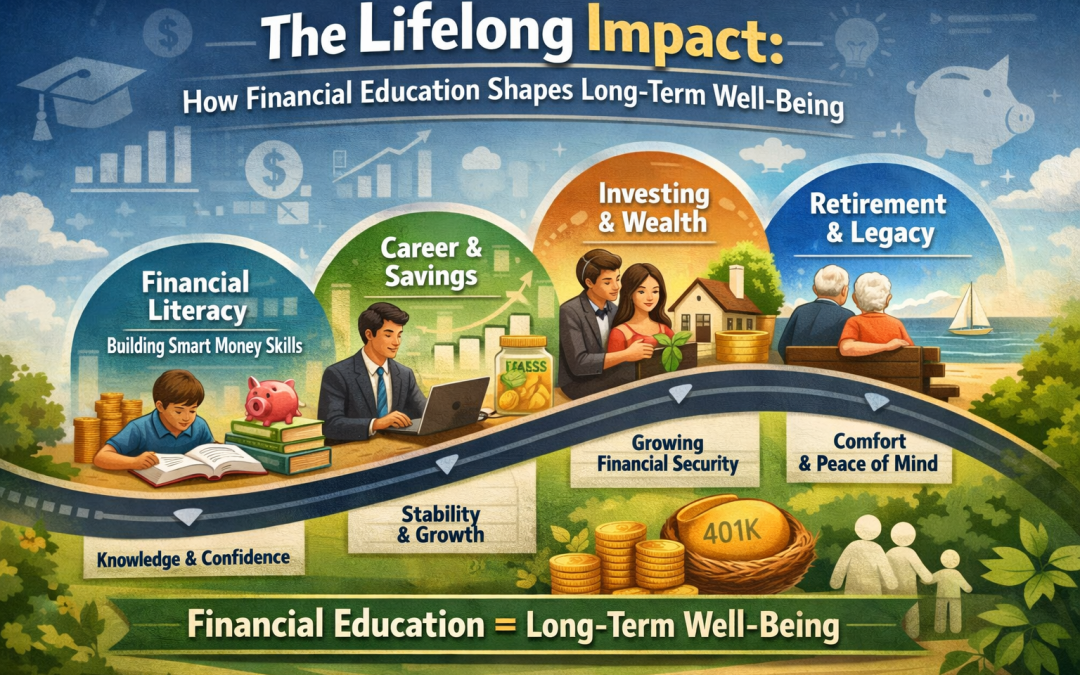

Introduction..

Financial education is often boxed into narrow conversations about budgeting or investing, but its true influence stretches much wider than spreadsheets.

When people gain basic financial knowledge (such as how to budget, use credit responsibly, save for emergencies, and plan for retirement), then that knowledge becomes a steady force that helps shape choices, opportunities, relationships, and also manages stress levels across a lifetime.

Therefore, financial education is not just about money; it is about a social and psychological investment that pays dividends in wellbeing.

Foundations: knowledge that prevents harm

At its most immediate level, financial education reduces weakness; namely:

- Knowing how to read a bank statement, recognise predatory lending, or distinguish between secured and unsecured debt gives individuals concrete tools to avoid costly mistakes.

- A family taught to maintain an emergency fund (even if it is very modest) is less likely to experience cascading crises when unexpected expenses arise.

- Similarly, understanding interest rates and compound interest prevents long-term damage from high-cost loans and unpaid credit card balances.

The above small pieces of knowledge compound (in both literal and figurative terms) over time. For example, avoiding a high-interest payday loan or steering clear of predatory contract terms can preserve capital that would otherwise be lost to fees and penalties. That preserved capital becomes the seed for future savings, investments, or educational opportunities.

Behavioural shifts: how learning changes habits

Financial education works not only by delivering facts but by reshaping behaviours.

Learning simple, repeatable habits, such as automated savings, monthly budgeting reviews, and tracking spending categories, builds routines that make healthy financial choices automatic.

When people set up an automatic transfer to savings on payday, they reduce the cognitive friction that would otherwise allow impulse spending to win.

These habits interact with human psychology.

Education that emphasises realistic, incremental goals and normalises setbacks helps people stick with plans. It reframes financial success as a process rather than an instant transformation.

Over the years, repeated good habits turn into stable financial behaviours that persist through job changes, family transitions, and market fluctuations.

Long-term security and mental health

Financial stability is tightly linked to mental health.

Chronic money stress contributes to anxiety, depression, and strained relationships. By lowering uncertainty (say as through emergency savings, retirement planning, and manageable debt loads), financial education reduces the everyday worry that wears down quality of life.

People who understand their finances are better positioned to make intentional life choices rather than reactive ones driven by reacting to short-term crises.

This security also impacts physical health. Stress has measurable effects on sleep, immune functions, and chronic disease risks. When financial education prevents repeated fiscal shocks or minimises lengthy debt repayment periods, it indirectly supports long-term health outcomes that will show up decades later.

Social mobility and opportunity

Financial literacy can be a lever for social mobility.

Knowledge about saving for higher education, evaluating housing affordability, or accessing low-cost capital for small businesses enables people to pursue opportunities they otherwise might sacrifice. For example, a prospective entrepreneur who understands small-business bookkeeping and financing is likelier to secure a loan with realistic terms and steer clear of unfair arrangements.

Moreover, financial education encourages informed use of institutional resources such as scholarships, tax credits, retirement accounts with employer matches, and government assistance programs. Knowing how to maximise these options can translate into more assets accumulated over time, which compounds advantages for future generations.

Intergenerational effects

Money habits and attitudes are often passed down within families.

When parents demonstrate sound financial behaviour and explain the reasoning behind saving and planning, then children will internalise these as norms, which will then shape their future decisions. Conversely, cycles of financial illiteracy can perpetuate vulnerability.

This means that investing in financial education is, therefore, a social multiplier. Its benefits extend beyond the immediate learner to siblings, children, and even extended family networks.

Programs that target young people by integrating age-appropriate financial topics into school programmes of study have a particularly high return on investment. Early exposure to basic concepts like budgeting, delayed gratification, and interest helps form responsible financial identities that carry on into adulthood.

Civic and economic resilience

On a community and societal level, higher financial literacy contributes to economic resilience.

Households that maintain diversified savings and avoid excessive leverage are less likely to trigger localised economic collapses when shocks occur. Informed consumers also pressure financial institutions to offer transparent, fair products, shifting markets toward better practices.

Financial education fosters more equitable participation in the economy. When historically excluded groups gain access to knowledge about credit building, homebuying, and retirement planning, the gap in wealth accumulation narrows over time. This has ripple effects on housing stability, educational attainment, and civic engagement.

Designing effective financial education

Unfortunately, not all financial education is equal.

The detailed and structured programmes that succeed share a few characteristics. For example, they are practical, culturally relevant, allow experimentation and are reinforced over time. This means that short, one-off seminars are far less likely to succeed.

Personalisation matters too. Financial advisors are now tailoring advice to life stage and income level is more actionable than generic tips.

Finally, behavioural nudges (such as setting default options for employer retirement contributions) add to education by making positive choices easier.

Conclusion: more than numbers

Financial education is a long-term investment in human prosperity because it reduces harm, builds productive habits, supports mental and physical health, expands opportunity, and finally strengthens wider communities.

Furthermore, it acts through both individual choices and social structures, meaning its benefits are durable and far-reaching.

When policymakers, schools, employers, and community organisations prioritise accessible, practical financial education, they are not merely teaching people how to balance a bank statement. They are helping shape decades of greater stability, autonomy, and well-being.

In the end, money is a tool, and education is the method that helps people use this tool successfully to build the lives they want.

Recent Comments